Most learner drivers assume that sitting in the passenger seat of a parent’s car automatically makes them covered. It does not. Getting learner driver insurance explained properly before you hit the road is one of the most important steps you can take as a new driver, and one of the most commonly skipped. Without valid cover, you are breaking the law the moment you move the car. You risk fines, penalty points, and even having the vehicle seized. This guide cuts through the confusion, covering your legal obligations, the types of policy available, what things cost, and the scams you absolutely need to avoid.

Table of Contents

- Key takeaways

- Learner driver insurance explained: legal requirements

- Types of learner driver coverage

- Cost of learner driver insurance: what affects your premium

- Risks and scams to avoid

- My take on learner insurance best practices

- Ready to learn with confidence?

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Insurance is a legal requirement | You must have valid cover before driving on public roads with a provisional licence, no exceptions. |

| Standalone policies protect the car owner | A separate learner policy keeps the car owner’s No Claims Discount safe if you have an accident. |

| Temporary cover has flexible durations | Policies are available from one hour up to 24 weeks, so you only pay for what you actually need. |

| Ghost insurance is a real and growing threat | Fraudulent policies sold via social media can be cancelled immediately, leaving you uninsured without knowing it. |

| Vehicle choice affects your costs now and later | Lower-powered cars sit in lower insurance groups, reducing costs during your learner period and beyond. |

Learner driver insurance explained: legal requirements

Before you can practise on public roads in the UK, you must hold a valid provisional licence and have insurance in place. There is no grey area here. The law requires every vehicle driven on a public road to be insured, and that applies to learner drivers just as firmly as it applies to anyone holding a full licence.

To be eligible for a learner driver policy, you generally need to meet the following criteria:

- Aged between 17 and 75

- Hold a valid UK provisional licence

- Be a UK resident

- Driving a vehicle valued under £50,000

- Be supervised by a qualified driver aged 21 or over who has held a full UK licence for at least three years

The supervision rule is not just a formality. Insurance policies for learners strictly require qualified supervision; any deviation from this invalidates your coverage. Even a short drive around the block without your supervisor present voids your policy completely and exposes you to prosecution.

The penalties for driving without valid insurance are serious. You face a minimum £300 fine and 6 penalty points, and a court can impose an unlimited fine along with a driving ban. The vehicle can also be seized on the spot. Starting your driving journey with six penalty points on your licence before you have even passed your test is a significant setback, since newly qualified drivers are subject to a two-year probationary period with a lower points threshold.

Pro Tip: Always keep a digital or physical copy of your insurance certificate with you whenever you practise. If you are stopped by police, you will need to produce it.

Types of learner driver coverage

Understanding your options is where most learners get confused. There are broadly two routes available to you, and each comes with genuine trade-offs worth thinking through carefully.

Adding yourself to a family member’s policy

This is the most obvious route and the one many families default to. A parent or guardian contacts their insurer, adds the learner as a named driver, and practice can begin. It sounds simple, but adding a learner to family insurance can increase premiums and, more critically, it puts the car owner’s No Claims Discount at risk. If you have an accident while named on their policy, any resulting claim counts against their record. That could cost them far more in future premiums than the original saving was worth.

There is also an administrative risk. Failing to disclose a learner driver to the insurer can lead to denied claims or the policy being re-rated entirely. If your family member forgot to inform their insurer, any accident you are involved in may result in no payout at all.

Standalone temporary policies

A standalone learner policy is legally separate from the car owner’s annual insurance. This matters enormously. Standalone learner insurance protects the owner’s No Claims Discount if you make a claim, because any claim is settled against your policy, not theirs.

Here is a comparison of the two main approaches:

| Feature | Named on family policy | Standalone learner policy |

|---|---|---|

| Car owner’s No Claims Discount | At risk if learner claims | Protected |

| Flexibility of duration | Fixed to annual renewal | Hourly, daily, weekly, monthly |

| Cost control | Depends on existing premium | Pay only for practice time needed |

| Speed of setup | Can take days via insurer | Quotes generated online quickly |

| Premium impact on owner | Usually increases their premium | No impact on owner’s premium |

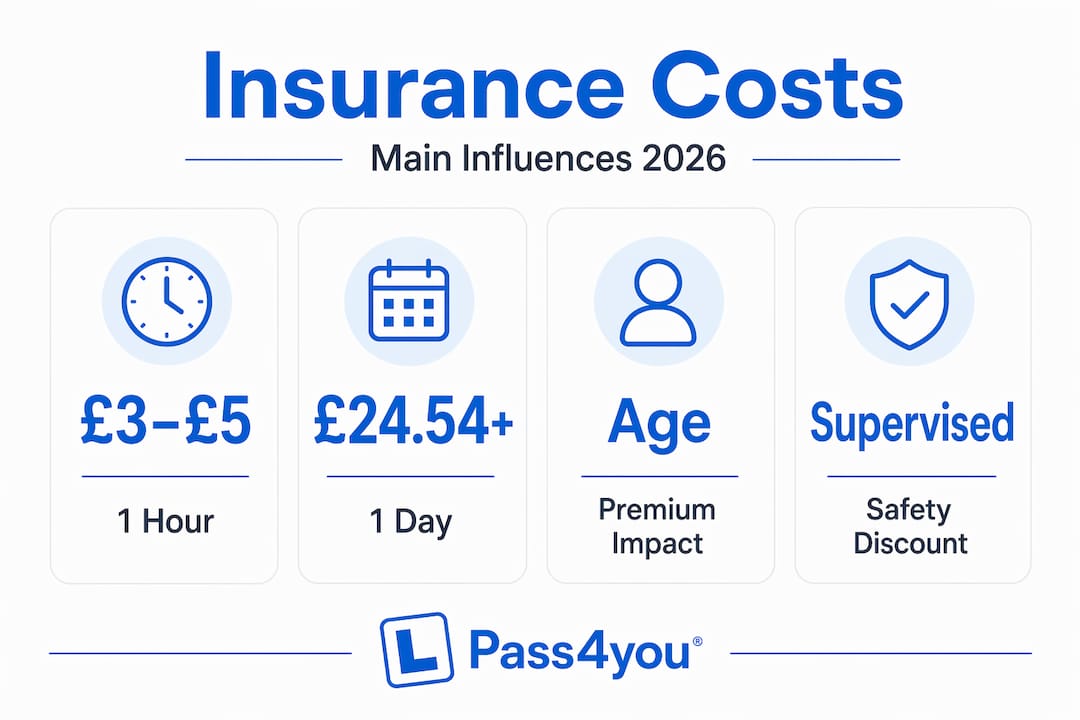

Temporary learner cover is available from as little as one hour up to 24 weeks, with standalone daily cover from approximately £24.54 per day, hourly cover typically running between £3 and £5, and monthly options costing between £60 and £120.

One important limitation to know: learner policies typically do not cover motorway driving unless you are accompanied by an approved driving instructor in a dual-controlled vehicle. Practising on a motorway with a family member under a learner policy is not permitted.

Pro Tip: Match your policy duration to your actual practice schedule. Matching insurance to practice needs prevents gaps in cover and stops you paying for days you are not even behind the wheel.

Cost of learner driver insurance: what affects your premium

Pricing is where learner drivers often have unrealistic expectations. The cost of learner driver insurance is influenced by several factors that you have more control over than you might think.

The table below shows typical price ranges by duration:

| Duration | Approximate cost |

|---|---|

| 1 hour | £3 to £5 |

| 1 day | From £24.54 |

| 1 week | £50 to £80 |

| 1 month | £60 to £120 |

| Up to 24 weeks | Varies by insurer |

Beyond duration, two factors carry the most weight. The first is your age. Younger drivers are statistically higher risk, so premiums reflect that. The second is the vehicle you are practising in. Choosing smaller, lower-powered cars significantly lowers insurance costs because they fall into lower insurance groups. A 1.0-litre hatchback costs considerably less to insure than a 2.0-litre saloon, both for your learner policy and for your first full policy once you pass.

This matters beyond your learner period. The habits you form now, including which car you choose to practise in, shape your insurance costs for years ahead. Starting in a modest, low-powered car is genuinely one of the best long-term financial decisions a new driver can make.

Here are practical ways to manage the cost of learner driver insurance:

- Get quotes from multiple standalone providers rather than accepting the first price you see

- Choose a car in a low insurance group for practice sessions

- Avoid modifying the practice vehicle in any way, as modifications push cars into higher insurance groups

- Consider shorter policy durations initially and extend only as your lessons progress

- Check whether completing a Pass Plus course after passing could reduce your first full premium

Pro Tip: Some insurers offer discounts for young drivers who can demonstrate supervised hours or who take additional safety training. It is worth asking directly when comparing quotes.

Risks and scams to avoid

Learner drivers searching for cheap cover online are a specific target for fraudsters. The most common threat is what is known as ghost insurance.

Ghost insurance scams sell fraudulent cover via social media with suspiciously low quotes. You receive what looks like a valid certificate, but the policy is either fictitious or is cancelled by the fraudster shortly after payment, leaving you uninsured without realising it. You could be driving legally in your own mind while being completely unprotected in reality.

“These scams can leave drivers uninsured with all associated legal risks. Verifying insurer legitimacy before purchasing any policy is not optional. It is the only way to protect yourself.”

To stay safe when buying insurance for learner drivers, follow these steps:

- Only purchase from insurers or brokers registered with the Financial Conduct Authority (FCA). Use the FCA firm checker at fca.org.uk to verify any company before you buy.

- Never buy insurance through social media direct messages, WhatsApp, or informal online groups.

- Check that you receive proper policy documents, not just a certificate, and verify the insurer’s contact details independently.

- If a price seems dramatically lower than all other quotes, treat it as a warning sign.

The consequences of unknowingly driving on invalid insurance are the same as driving with no insurance at all. The law does not distinguish between deliberate and unwitting offences. You will still face fines, penalty points, and potential vehicle seizure. Protecting yourself starts with where you buy, not just what you buy.

My take on learner insurance best practices

I have worked with learner drivers at all stages of confidence and preparation, and one pattern I see repeatedly is that insurance gets treated as a box-ticking exercise rather than an actual decision. That approach consistently causes problems.

In my experience, adding a learner to a parent’s policy sounds like the easy option, but it often is not the right one. When I see families go down that route without thinking through the No Claims Discount implications, the fallout from even a minor bump can be financially painful for everyone involved. A standalone temporary policy, even if it feels like extra effort, almost always offers more protection for the car owner and more flexibility for the learner.

What I find equally frustrating is how often learners miscalculate how much practice time they actually need. They buy a week’s cover, run out, and then squeeze in a few unsupervised sessions assuming it will be fine. It will not be fine. All practice must be supervised; even a brief solo drive is illegal and voids any insurance entirely. Being honest with yourself about your timeline and buying cover to match it is not just about money. It is about staying legal.

My straightforward advice: use legitimate providers, choose standalone cover where possible, and treat insurance duration as something to plan rather than something to improvise.

— Simon

Ready to learn with confidence?

Understanding your insurance options is the first practical step. The next is making sure the time you spend behind the wheel actually builds the skills you need to pass.

At Pass4you, we work with learner drivers in Milton Keynes and the surrounding area to build genuine confidence and road-ready skills. Our learner driver courses are designed around your pace, using modern dual-controlled Volkswagen vehicles and calm, experienced instruction. With an 83.33% first-time pass rate, well above the local average, our approach works. If you want to get test-ready efficiently, our intensive driving courses are structured specifically for learners who want to progress quickly. The better prepared you are, the shorter your insurance costs run too. That is a practical win all round.

FAQ

What is learner driver insurance?

Learner driver insurance is a specific type of policy that provides legal cover for drivers who hold a provisional licence and are practising on public roads. It can be set up as a standalone temporary policy or by being added as a named driver on an existing policy.

How much does learner driver insurance cost?

Hourly cover typically costs between £3 and £5, daily cover starts from around £24.54, and monthly policies range from £60 to £120. Costs vary depending on your age, the vehicle, and the insurer.

Does learner insurance cover the supervising driver?

No. Learner insurance covers only the learner; the supervising driver is typically covered by the car’s annual policy. You should confirm with the car owner that their policy permits them to supervise a learner.

What happens to my insurance after I pass my test?

Most learner policies include a short grace period, usually around three hours, allowing you to drive home after passing. After that window closes, you need a full driving licence policy in place before getting behind the wheel again.

How do I avoid ghost insurance scams?

Only buy from FCA-registered insurers or brokers, and verify any company using the FCA firm checker before purchasing. Avoid buying cover through social media, and treat any quote that is dramatically cheaper than competitors as a potential red flag.

Leave a Reply